Abstract

Markets are often explained as reacting to discrete news events, yet many price movements unfold gradually, even when little new information appears. This research note examines narrative momentum as a mechanism of how expectations form: the process by which a dominant interpretation persists and shapes how subsequent information gets read, driving market behavior long after the initial facts are known.

Narrative Momentum

Narrative momentum refers to the persistence of an interpretation once it becomes dominant. The momentum comes from coherence and wide adoption, not from the interpretation being correct. The mechanism works in three stages:

- Initial framing: An event introduces a plausible interpretation, one that fits the context people are already working with.

- Reinforcement: That interpretation gets repeated across commentary and coverage, applied to new data points, and gradually becomes the lens through which everything that follows gets read.

- Expectation shift: Beliefs adjust because the narrative has become the dominant signal. New information gets processed through the frame rather than on its own terms.

Narratives also collapse, and when they do they tend to break faster than they formed. That is why the corrections that follow dominant narratives are often sharper than the buildups that preceded them.

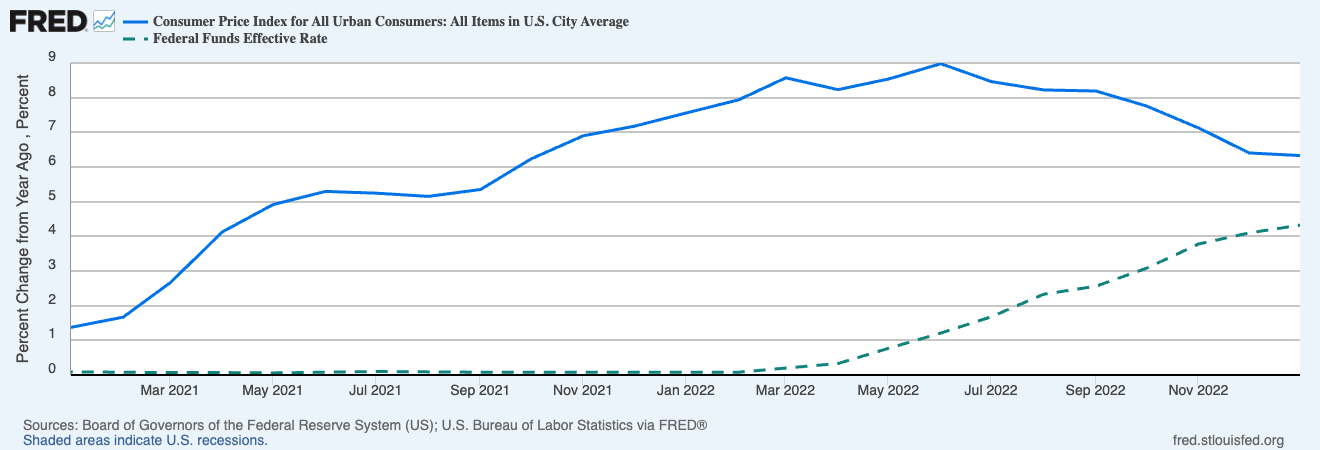

The Federal Reserve and Transitory Inflation (2021–2022)

When inflation began rising in early 2021, the Fed chose interpretation over action. Chair Jerome Powell introduced the word "transitory" to describe the price increases, framing them as a temporary artifact of pandemic disruptions rather than a structural shift. The argument was defensible at the time, as supply chain disruptions were real and the data was genuinely ambiguous.

What followed was more than a central bank holding a reasonable view under uncertainty. The transitory framing was repeated across Fed communications and adopted by Treasury officials, reinforced by economists who found it plausible. Markets priced accordingly, with rate expectations staying low and bond markets reflecting a belief that inflation would resolve without intervention. Each month that inflation remained elevated was reinterpreted through the same lens, still transitory, just taking longer than expected. By late 2021, the frame had become self-reinforcing, sustained less by data than by the authority of the institutions repeating it, which is why dissenting views struggled to gain traction.

When the Fed pivoted in early 2022, acknowledging that inflation was persistent, it triggered one of the fastest rate hiking cycles in decades. The S&P 500 fell roughly 20 percent in the first half of 2022, bond markets repriced sharply, and the delayed intervention contributed directly to the severity of the correction that followed.

Limits and Caveats

Narrative momentum is difficult to measure cleanly and risks ex post interpretation. In the transitory inflation case, one could argue the Fed was making a reasonable forecast under genuine uncertainty rather than being captured by its own framing. The line between a considered institutional judgment and a dominant narrative that has stopped absorbing contradictions is rarely clear from the outside, and distinguishing between the two empirically remains a genuine challenge.

Closing

Tracking headlines is the least useful way to understand how markets are moving. The more useful question is which interpretations are gaining coherence, which are beginning to absorb contradictions that should be challenging them, and which are approaching the point where the frame can no longer hold. The narratives that matter most are rarely the ones that arrive with a single decisive headline. They are the ones that build quietly, shape how everything else gets read, and eventually break in ways that look obvious only after the fact.